IRFC IPOs: India's Bureaucratic AerCap

Plus: Why I usually never invest in an IPO; My love-hate relationship with government owned enterprises; and Reading filings

IRFC's IPO

Two secular trends which are intensifying in India, the world's third largest economy and, till 2020, the fastest growing. The first is privatization of government enterprises and the second is the expansion of the railway infrastructure in the country.

Investors have benefited tremendously when these trends converge and present themselves in the public markets (RVNL, IRCTC, RITES among others). Another such opportunity has made itself available.

The Indian Railway Finance Corporation (IRFC) is currently offering fresh and secondary shares for sale in its IPO. The company is an intermediary between the Indian Railways, the Ministry of Railways, and institutional investors. It raises capital for the purchase of Rolling Stock assets and then leases them, owns & leases Project Assets of the Indian Railways and lends to other organizations under the ministry umbrella.

IRFC at its current offer price offers an opportunity similar to the one in AerCap NV after the March 2020 market crash. The allotment price also offers attractive call options for free. Let's dive in.

The Moat

By virtue of being a government owned enterprise, IRFC has near complete monopoly over the Indian Railways’ capital market financing and asset leasing. This is a very attractive business for reasons outlined below. 20-25% of the Railways' capital is raised by IRFC, and 100% of its debt is either raised by or passed through it.

It is one of the very few companies in India to be rated equal to the sovereign debt rating. This leads to a low cost of borrowing (Note: The Modi government currently in power is brilliantly reducing spending, increasing revenue and lowering its deficit. This has led to an improvement in the credit quality and repayment ability, however the rating agencies are yet to upgrade their assessment.)

IRFC has the privilege to issue tax free bonds, which also reduces its cost of borrowing. This leads to a low cost of debt and a low discount rate.

The government infuses capital into IRFC at a very low cost of equity (mostly dilution via rights issues and dividends). I would not be surprised if the company had the lowest cost of capital among peer financial institutions and this bodes well for its financing operations.

One of the two biggest competitive advantages the company has is that the Ministry of Railways guarantees all debt repayments and will cover them if needed. This has not happened and I believe it won't, but it reduces the cost of capital even further. Very rarely do you find a lessee covering the lessor's obligations.

The other competitive advantage is the Railway Ministry looking after procurement, maintenance, expansion and repair. This is an advantage I believe even AerCap or other lessors don't have. This leads to higher Free Cash Flow (no capex) and a higher return on invested capital. The company is a pure play financier, with only financial assets due to this clause in its lease agreement.

The Upside

Despite having one of the largest rail networks in the world, India has one of the lowest route kilometers per land area, per capita and 65% of its routes run at greater than 100% capacity. The government has acknowledged this and has started updating its rail infrastructure.

Some notable projects include Dedicated Freight Corridors, doubling and electrification of lines, security infrastructure, high speed rail among others. All of these will directly or indirectly benefit IRFC. Rolling Stock will be financed by the company directly and it will be the nodal lender to government SPVs operating in the other sectors above. I would like the share of intergovernmental lending to go up as it is higher margin with the same low risk as the low margin lending to the Railways.

The company receives a 30 basis point spread over its leases from the Railway Ministry. This fixed margin provides stability for modeling but doesn't fare well for growth in profitability or returns on capital. However, the volume expansion ongoing is enough to be the growth engine for the company along with the other agency lending described above. As an example, LIC has decided to provide $20 billion in financing to the Railways, most of which will pass through IRFC.

Government companies in India are infamous for their lack of prudence and low efficiency. IRFC bodes well on these two factors, it is the best in its peer group of listed government companies when judged on these metrics. It has 26 employees, which is marvelous as government companies often have employees bursting from the seams.

The company has not provided a detailed capital and asset structure yet, which is why I cannot comment on their long term cash flow potential without studying it first. However, the short term liquidity coverage is good.

The company has substantial dry powder to deploy, and infrastructure expansion will provide it with good opportunities. The company is like the investment bank for the Indian Railways, but it has not yet captured the full financial value chain yet. Due to fears of private and foreign control, equity raising has not yet been tried in railway projects. IRFC has not tried to advise or market the railways in transactions other than debt raises. I believe that is set to change, which will unlock profitable revenue streams.

The company has a net interest spread of 80 basis points, which is heavily dependent on interest rates. The Reserve Bank will increase rates at some point, probably 2025, after the general elections, because the growing Indian economy will overheat and because the RBI is prudent unlike the Fed and its coterie. The management is good and will steer the company well.

The Downside

The risks to IRFC are the same risks every government company has: red tape, bureaucracy, inefficiency, no skin in the game, among other things. Public oversight will prevent this from happening after the IPO, but we can never be too sure.

If the Ministry of Railways lowers the margin paid to IRFC below ~20 bps, the company ceases to be profitable. This is a huge risk, and the company needs to diversify as 97% of its revenue is from the ministry. Not including hedging costs in the lease agreement costs would be harmful as well.

Growing competition is a risk too, but not a big one. Until the government privatized IRFC, it will retain its monopoly.

Something I see no one observing is IRFC not investing its ‘float’, at all. Everybody knows finance and insurance companies can generate a lot of capital, which when allocated properly can do wonders. Look at Berkshire, White Mountain, even LIC. This is something to keep an eye on.

Management leaving would be detrimental, and improper hiring would have adverse effects. This is another thing to watch.

The most important risk is a change in government or economic conditions. Even if your thesis is correct, events outside of your control can flip it on its head. Look at how Daniel Sundheim got burned on his PNB thesis.

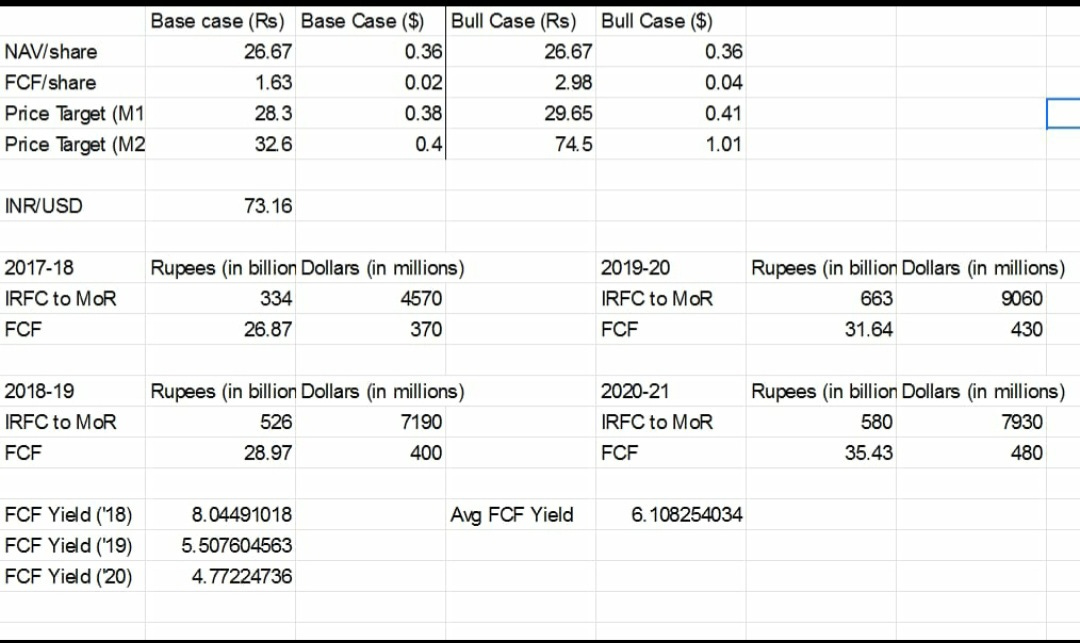

The Valuation

I have a base case and bull case. My valuation uses Net Asset Value + next year's Free Cash Flow (Operating Profit - Capex). For the base case I use this year's FCF, for the bull case I use 3 year incremental FCF margin to calculate next year's cash flow. The second methodology for the base case is 20 times Free Cash Flow, for the bull case is 25 times FCF. This is conservative for a company with a 25% margin, 25 to 30% FCF margin and 5-9% FCF yield on loans.

The prospectus filed by IRFC can be found here. The Net Asset Value and FCF per share are sourced from this document. I would have preferred to calculate my own net asset value but no complete breakdown of assets is given.

Whether you should invest or not is up to you. I trust readers who've made it here to use their faculties well and decide on a course of action which leads to great risk adjusted returns with no permanent impairment of capital. I don't want a reader to wake up one day and find a hype, overvalued stock in their portfolio, even if it has earned them outlandish returns.

Personal disclosure: I have applied for share allotment.

I encourage you to do your own research, and, if you want to, share it with me. Investors familiar with aircraft leasing cos will find something similar yet fresh and those not familiar with India will be introduced to a whole new world.

IPOs

I usually never apply for any IPO, as the marketing of machine of the local Wall Street gets into gear, and the incentives aren't aligned. The fear of missing out can overwhelm your rational faculties and lead to regretful decisions.

An undersubscribed IPO would be the holy grail, which I would buy into enormously. I don't have much data to back my claim but I believe undersubscribed IPOs will generate tremendous returns. The Infosys IPO is one such example, I'm sure there are others.

Government companies

The tragedy and beauty of these companies is that they can be as big as Apple but never will, with the exception of Aramco and other oil companies. When you think about it, they have a low cost of debt, low cost of equity, incomparable capital, and the backing of a sovereign. The added advantage in India is the smartest people want to work for the government. You could follow the Sergei Witte model and grow your economy at 10% +.

All of this potential is unfortunately wasted. There is much to write about this which could be a whole other newsletter. As a value investor, I like SOE stocks because they're always undervalued. As a human being, I hate their bureaucracy.

Reading filings

When you decide to be a value investor it is implicit that you will be spending most of your day reading something, and a large %age of your time will go towards reading filings. You have to be nuanced when doing this, not getting coaxed by marketing speak and fancy presentations, while not going senile when reading government filings and documents.

You have to be neuroatypical or comfortable with being bored if you want to do this. Two examples are Norbert Lou and Michael Burry. It's best to have an assistant or analyst do this, as you will lose your sanity or social life somewhere along the way as your stock universe scales. I'm not there yet but I'm still overwhelmed.

I believe, very strongly, that you will have found my maiden endeavour into published security analysis interesting, whether you agree or disagree with my conclusions. Please reach out to me if you have comments, do subscribe and share with your acquaintances.

HI skand,

Nice write-up. One aspect which you have ignored is the dividend which this company has not declared and is supposed to declare soon. As mandated PSUs are supposed to declare 30% or profits as dividend which will amount to Rs.1.10 to 1.30 and incremental in future also.

that itself would amount to a yield better than savings account even if the IPO lists at 26/-

please mail me your comments at amit264agarwal@gmail.com

would love to connect with you .

reagrds

Thanks. Would help to know your thoughts on government spending/fisc